Climate Risk

refinq

-

Crunching the Numbers: Why Ignoring Climate Risk Could Cost Your Business Big

Global natural disaster losses are rising rapidly, with 2023–2024 marking record levels of insured and economic damages driven by severe thunderstorms, floods, and secondary climate hazards. These “non-peak” events now account for a majority of global losses, reflecting shifting risk patterns amplified by urbanization, aging infrastructure, and climate change. This article explores the growing financial impact of natural catastrophes, the limitations of traditional risk models, and the importance of high-resolution, location-specific climate risk assessments to support resilience and informed decision-making.

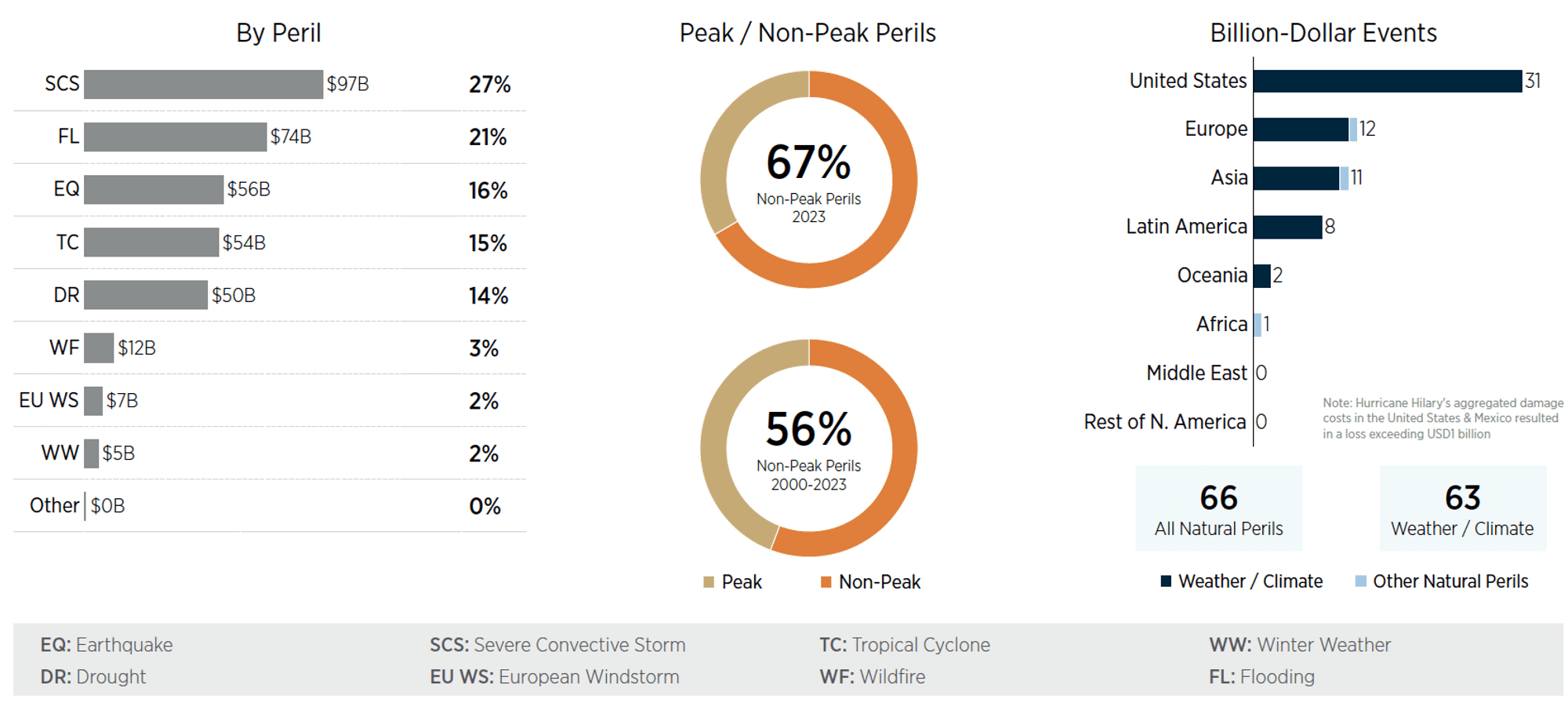

The world is experiencing an unprecedented surge in natural disasters, with the financial toll reaching staggering heights. The first half of 2024 alone has seen a record-breaking spike in insured losses, primarily driven by severe thunderstorms that wreaked havoc across the United States. These storms caused a jaw-dropping $42 billion in damages, a massive 87% increase compared to the average of the past decade (1).

Floods have also played a significant role in this devastation, with major incidents in the UAE, Germany, and Brazil causing billions more in damages(1). The year 2023 was no better, with natural disasters racking up a staggering $357 billion in global economic losses—a 4% rise from the previous decade and a 14% spike compared to the entire 21st century (2).

A particularly concerning trend is the escalating frequency of "secondary" natural disasters, such as severe thunderstorms, flash floods, and wildfires. These events are now inflicting greater economic damage than the traditionally more intense "peak" disasters like hurricanes. These secondary hazards, which were previously underestimated, have become the new standard, exerting significant strain on infrastructure, economies, and communities. In 2023, non-peak perils accounted for two-thirds of total loss costs, an 11% increase compared to the 21st century average(2).

This worrying trend appears to be accelerating. As global temperatures rise and populations gravitate towards urban centers, the threat of catastrophic events is escalating. Population growth, especially the concentration of people in coastal areas and the expansion of the wildland-urban interface, is a major contributor to the increasing losses (3). This demographic shift has resulted in a significant rise in the number of properties vulnerable to natural hazards. By 2050, the WUI population in some U.S. regions is projected to grow by up to 40%, further exacerbating the problem (4).

Moreover, the changing nature of the built environment exacerbates the problem. As cities expand and older infrastructure ages, they become more vulnerable to extreme weather events. For instance, the proliferation of solar panels in hail-prone regions(5), or the aging of urban drainage systems unable to cope with heavier rainfall, highlights these vulnerabilities.

Moreover, conventional approaches to quantifying economic losses frequently disregard the impact of rising property values and construction costs. This can lead to a distorted understanding of the true financial ramifications of natural disasters.

The Importance of Climate Risk Assessment

Generic risk assessments offer a broad overview, but they fall short in providing the granular insights businesses need to make critical decisions. In today's climate crisis, a one-size-fits-all approach is insufficient.

refinq: Your Partner in Climate Resilience

refinq provides a sophisticated, location-specific climate risk assessment solution. By merging hyperlocal data and advanced modeling, we offer businesses the insights necessary to navigate climate risk challenges.

Regulation-Ready Assessments: Our assessments align with the EU Taxonomy, ensuring compliance and future-proofing your business.

A 3-Step Process to Success: We simplify complex risk management into clear, actionable steps:

Identifying specific climate risks for your location.

Assessing your vulnerability to those risks.

Developing tailored adaptation strategies.

Unmatched Granularity: Our high-resolution analysis provides insights down to the individual site level, empowering informed decision-making.

Future-Proof Planning: We leverage cutting-edge climate projections to help you anticipate future risks.

Data-Driven Confidence: Leveraging cutting-edge scientific data, including Copernicus, World Bank, and IPCC CMIP6, our assessments deliver reliable and actionable results.

Empowering a Resilient Future

With refinq, you can transition from reactive crisis management to proactive risk mitigation. Protect your bottom line, make informed investments, and demonstrate your commitment to sustainability.

Don't let natural disasters catch you off guard. Take control of your business's climate risk today. Contact refinq to learn how our hyperlocal climate risk assessments can help you build a resilient future.

References:

https://www.guycarp.com/insights/2022/07/is-climate-change-to-blame-for-increasing-losses.html

https://www.communitywildfire.org/wp-content/uploads/2021/02/CWPC_Land-Use-WUI-Report_Final_2021.pdf

Cover Image: Pixabay on Pexels